The closing weeks of 2005 saw a deluge of dastardly revelations in the press about the questionable practices of NKF and its CEO TT Durai. The source of much public ire was the long awaited "A Report on The National Kidney Foundation" dated 16 December 2005 by the KPMG investigation team which contains such entry:

"6.11 High gross profits earned by the NKF on chargeable drugs

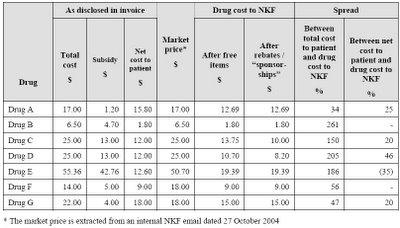

6.11.1 The NKF reported in its Investment Report 2004 that it enabled its patients to save in excess of $3.5 million in treatment costs by providing subisdies for costly medication and by bringing down drug prices.

6.11.2 We found that the amount of such savings was derived from the difference between the prices charged by NKF and a notional market price of drugs based on estimated annual consumption in 2004 instead of the difference between the prices charged by the NKF and the actual prices of drugs paid by the NKF. These savings were reflected in invoices given to patients. (see table)

6.11.3 We found that the stated cost of drugs dispensed to patients as reflected in the invoices closely approximated the market price of the drugs.

6.11.4 As mentioned above, the market price was a notional market price determined by the NKF. The NKF, being a substantial and significant purchased, enjoyed subsidies and rebates from its drug suppliers. Instead of passing these costs savings to its kidney patients, we found that the NKF charged its patients a premium for certain drugs."

On 21 Dec 2005, a Mr Subramaniam volunteered to explain in the Straits Times that the way the NKF treated the definition of subsidy and the way KPMG did were from"different perspectives".

The NKF defined subsidy as the difference between the amount a patient would pay for treatment and drugs elsewhere in Singapore and the amount they paid the NKF. "In my understanding of NKF's view, subsidy must be tested against the market rate and not the net amount incurred."

The logic is not new, as it was first introduced to a hapless public a year earlier by civil servant Desmond Wong who wrote:

HDB pricing keeps new flats affordable to most Singaporeans (ST Aug 6, 2004):

I REFER to the letters, 'What goes into pricing of HDB flats' (ST, July 23) by Mr Hiong Kum Meng and 'Subsidy should be based on flat's building cost' (ST, July 27) by Mr Mohamed Rafiq Hamjah.

Mr Hiong concluded that the increase in HDB resale prices has outstripped wage growth, based on a comparison of changes in the Resale Price Index with changes in average nominal wages between 1993 and 2003.

We would like to explain that resale flats are transacted in the open market on a willing buyer-willing seller basis. The prices are not set by HDB. Prices can fluctuate, depending on factors such as the economic outlook, employment situation and sentiments in the property market.

What is important is that HDB prices its new flats so that the majority of Singaporeans can afford one. From 1993 to 2003, the prices of new four-room flats increased by 2.6 per cent per annum, below the annual increase of 5.3 per cent in average wages cited by Mr Hiong. New-flat prices did not rise as steeply as resale-flat prices, because HDB prices new flats below their equivalent market price, that is, at a subsidy.

Mr Mohamed asked why HDB's subsidy for new flats is related to the market price and not the building cost of a flat. Today, first-time HDB flat buyers can buy either resale or new flats. Those who opt to buy resale flats from the open market can take up a housing grant of $30,000 or $40,000, which allows them to enjoy a discount off the market price of the flat.

Those who opt to buy new flats from HDB also enjoy a discount off the equivalent market price of the flat.

The difference between what the buyer pays HDB for his flat and what it is actually worth in the market is a direct and real subsidy provided by HDB to the buyer.

Like the housing grant for resale flats, the provision of such a market-related subsidy in the case of new flats has enabled HDB to keep its flats affordable for the majority of Singaporeans.

DESMOND WONG

Deputy Director (Marketing & Planning)

for Director (Estate Administration & Property)

Housing & Development Board

It hadn't always been like this. HDB had a nobler beginning.

The Housing Development Board was established by the first People's Action Party (PAP) government on February 1, 1960, to provide low-cost public housing. The Lands Acquisition Act of 1966 granted the Board the power of compulsory purchase of any private land required for housing development. The prices paid by the board were about 20 percent of the estimated market value of the land, which was in fact if not in form being nationalized. Between 1960 and 1979, the percentage of land owned by the government rose from 44 to 67 percent, increasing the government's control over that scarce resource and benefiting low income voters, who supported the PAP, at the expense of the much smaller number of private landowners. Rents for Housing and Development Board apartments were subsidized, and selling prices for the apartments were set below construction costs and did not include land acquisition costs. Purchase prices for HDB apartments in the 1980s were 50 to 70 percent below those of privately owned apartments.

{kind=link}

About Me

- Tattler

- "There is nothing to prevent you from pushing your propaganda, to push your programme out either to the students or with the public at large... and if you can carry the ground, if you are right, you win. That's democracy. We're not preventing anybody" ~ Lee Kuan Yew, 31 January 2005